|

|

|

The Gold (and Silver) bull continues to closely follow the giant wave formation of a tsunami. The recent more parabolic rise in Gold up to above $1,900 is analogous to the little ridge

of water we first saw way out in the distance, and now, much like when

the waters recede from the shore early in the tsunami wave formation,

Gold is undergoing a correction.

As the “Gold” waters receded, the diehard deflationists have run out onto the bare sea bed to whoop and holler that the sea of Dollar Inflation is ending. They

currently hop about the nearby sea floor waving their arms in victory

as they envision a catastrophic deflationary depression that will wreck

the financial market back to the Stone Age, and the price of the

Precious Metals along with it. Unfortunately,

they fail to understand the wave cycle at work as the waters are sucked

away from the shore only to strengthen the Gold tsunami wave that grows

in the distance For the great Gold tsunami wave is being bolstered as

the economy deteriorates, thereby necessitating a continued parabolic

growth of printing of paper currencies worldwide. Where

the first little parabolic rise in Gold merely caught the attention of

the public, the growing strength of that wave as it reaches shore will

leave everyone running for the hills of Gold and Silver.

The Fed Shows Inflation When They Want To and Deflation When They Want To

Last

week, the Fed met for a special two-day meeting that ended with a dull

thud as they announced “The Twist” that sounds a bit like a dance from

the 60s. They also stated that

the economy was weakening - economic weakness that has motivated them to

aggressively inflate the US Dollar for 10 years, now. Yet,

market expectations were for the Fed to announce another round of

Dollar Inflation via QE3 at the special 2 day meeting so the markets

sold off in response to the failure of the Fed’s announcement.

What

occurred in the Precious Metals markets seems a bit absurd as Gold and

Silver were pounded aggressively lower in price though the Fed often

leads rounds of Dollar Inflation with suggestive hints of deflationary

pressures. To some extent it

defines the need for their move, and it probably intends to show that

they are in control of something that they cannot control. The massive deflationary backdrop of debt demands that they either “inflate or die.”

Commentators

noted that the exaggerated fall in Gold, Silver, and in the PM stocks

resulted from margin calls “where investors sell what they have to

sell.” Yet, the extent of the

weekly fall in the DJIA was rather small compared to the 2 week fall

back in early August - a time when Gold, Silver, and the PM Stocks moved

higher. A more likely cause for

the fall in the PM sector lies in the Fed’s failure to announce QE3 as

it pointed to economic weakness, combined with this coming Tuesday’s

Gold and Silver options expiration date - a monthly bashing that

generally sees Gold and Silver whacked to lower levels. Further

downside pressure on the PM sector probably stems from big trading

firms reversing their “long Gold/ short PM stock ratio trade.” The

large swings in the Gold price over the last 30 days provided the

volume they needed to sell paper gold, and to cover and accumulate the

Gold and Silver shares. Given

the timing one has to wonder whether these large traders are the same

firms who trade for the Market Stabilization Fund, and if they knew in

advance that the Fed would tip its comments to deflation this week.

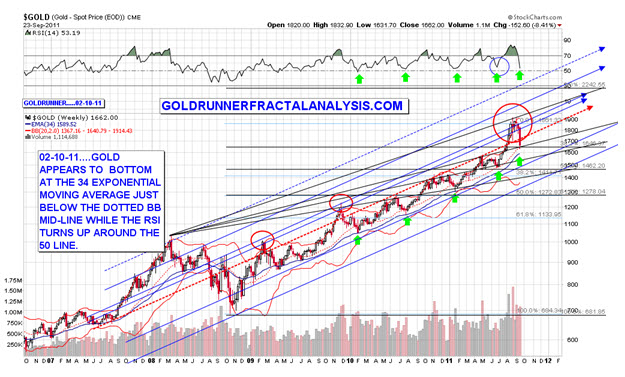

The Gold Chart

The

following Gold Chart shows that the cyclical tendency since early 2009

has been for Gold to bottom at the green arrows with Gold correcting

down to and through the dotted Bollinger Band (BB) mid-line to hit the

34 week exponential moving average while the RSI Indicator approaches

the 50 line. Gold fell to the BB mid-line on Friday as the RSI approached the 50 line. Black rays off of the 2008 top show that Gold has been bottoming at each black line extended over the “last top.” Gold reached that juncture on Friday. We might see Gold weakness early next week, but we expect the basic relationship to hold. Near this point in the 70’s Gold Chart, an imminent bottom produced a sharp rise.

REVIEW OF OUR EXPECTATIONS

1) A major bottom for the PM stock indices is now in place as we laid out for subscribers (see HERE for subscription details) early in the week of August 8th based on the fractal relationship to 1979.

2) Price

and the technical Indicator readings for the PM Stock Indices continue

to track the 1970’s with much higher prices expected in the

intermediate-term. Per the 70’s PM Stock Model we expect this run to be

the first, and smallest, of 3 momentum runs to come for the PM stock

indices over the next few years. The mid-900s appear to be a realistic target for the HUI Index into year-end, or into early 2012.

3) We have reached the point in the cycle where leverage returns to the PM stocks with a vengeance per the late 1970s charts.

4) The fundamentals for Gold, Silver, and the PM Stocks could never be better. In

fact, the Fed’s announcement this week was read as “deflationary”,

where in reality it screamed, “We must launch an accelerated program of

Dollar Inflation, and soon!”

5) Gold

has now corrected in a very similar time sequence to the late 70’s,

though the depth of the correction has been deeper over the last 2 days.

Current Gold price

relationships to the Bollinger Band mid-line and 34 EMA line suggest

that an intermediate-term bottom is likely due this coming week. Such a bottom would fit the 70’s model nicely.

6) The

US cannot pay its “regular bills” and interest on its debt, based on

its current cash flow, much less cover other important needs that are

growing astronomically. We now depend on the Fed printing an accelerating number of Dollars. This is what QE is - pure debt monetization that devalues the US Dollar aggressively. For the U.S. economy, it is either “print or die.” We

expect that the Fed will print while acting like they have some choice

in the matter other than a total Deflationary Depression. This fact has been true since early last decade.

7) The

Fed generally appears to prefer to see the prices of Gold, Silver, and

the Commodities correct to create overhead resistance on the charts

before they announce Dollar Inflation moves. That

is probably what was intended via the announcement at their special

2-day meeting creating the exaggerated fall in the PM sector this week -

coupled with the usual sharp weakness going into Gold and Silver

options expiration, next Tuesday.

8) With

the big funds ending the long Gold/ short PM stock ratio trade, the PM

stocks should be heavily supported after this bottom is complete.

9) The long-term PM Stock Model from the 70’s suggests that we will be entering the “sweet spot” of a 3rd Wave advance as soon as this correction is over.

10) Our upside targets for Silver for this run into late 2011/ early 2012 of $52 to $56 should be achievable for silver, with $58 to $62 as real possibilities.

11) We still expect all of our intermediate upside price objectives for Gold to be reached by late this year, or early next. We expect the next run in Gold to reach the $2250 level and $2500 level before a higher run takes us up to $3,000 Gold, or higher.

12) The

recent exaggerated decline in the PM sector will likely act like

pulling and letting go of a huge rubber band in terms of how the PM

sector will advance after this correction ends.

13) An

end of the aggressive and accelerating course of US Dollar Inflation at

this time by the Fed would create a deflationary depression that would

dwarf that of the 1929 era yet the Fed has gained the right from

Congress to inflate to infinity if necessary. That

right is the major difference between today and 2008 when nobody could

foresee the Fed moving to aggressive Dollar Inflation via debt

monetization after they blew out the banking multiplier loan system of

Dollar Inflation. Debt

monetization, QE, is a more permanent form of Dollar Inflation that

cannot easily be reversed, thus the Dollar Devaluation via QE will be

mostly permanent leaving a more permanent high price of Gold when it is

all over.

14) We believe that we lie at a “load the boat moment” in this historic Gold and Silver bull for Gold, Silver, and the PM stocks.

Summary

1. The mid-900s appear to be a realistic target for the HUI Index into year-end, or into early 2012.

2. $52 to $56 should be achievable for silver, with $58 to $62 as real possibilities, by late 2011/ early 2012

3. The

next run upward in Gold to the $2250 level followed by $2500 with the

potential for $3,000, or a bit higher, is now on the radar screen for

late this year, or early next.

Source: http://news.goldseek.com/GoldSeek/1317000203.php